Construction buyers report shows growth

This post has already been read 1087 times!

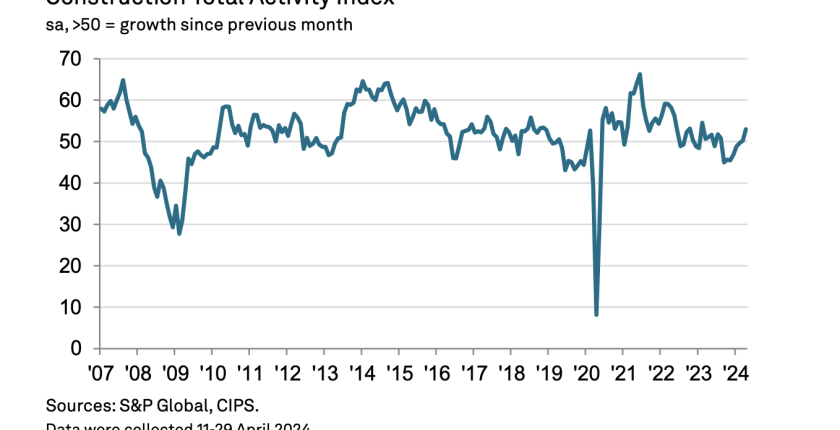

Construction has been in the doldrums over the past year but the construction buyers report is rising at its fastest pace for 14 months which shows an upward trend.

The report from the bellwether S&P Global UK Construction Purchasing Managers’ Index rose to 54.7 from 53.0 in April the fastest rate growth rate in two years.

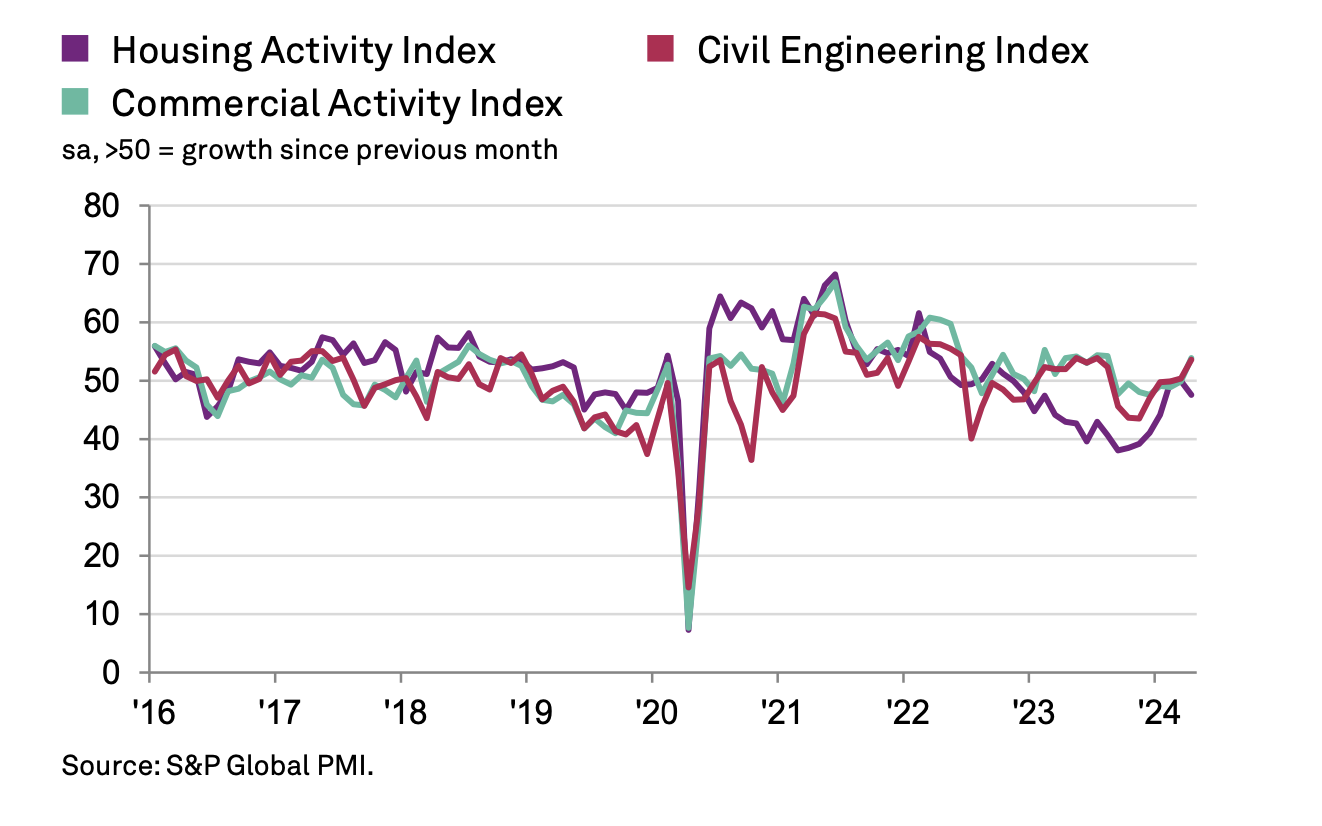

The three main monitored categories of house building, commercial and civil engineering saw activity increase for the first time since May 2022 and new business rose for the fourth consecutive month, and at a solid pace that was the fastest for a year as demand conditions improved. Many delayed projects have restarted and firms are winning new contracts which has helped with the growth.

Tim Moore, Economics Director at S&P Global Market Intelligence commented saying that.

“The construction sector consolidated its recent return to growth in April, with total industry activity rising at the fastest pace for 14 months amid an ongoing recovery in order books. Demand was boosted by greater confidence regarding the broader UK economic outlook. Commercial construction outperformed in April and civil engineering also provided a solid contribution to overall growth.

“Lacklustre market conditions in the house building segment continued to weigh on activity. The latest survey pointed to the fastest reduction in residential building work since January, although the speed of the downturn remained much softer than in the second half of 2023.

“Hiring trends were subdued in April despite a recovery in workloads, which mirrored trends seen in other part of the UK economy, as construction firms sought to maintain a tight focus on costs against a backdrop of strong wage pressures. Purchasing prices nonetheless increased only modestly in April. An improved balance between supply and demand helped to contain overall input cost inflation, as suggested by the fastest improvement in vendor performance so far in 2024.

“Business activity expectations for the year ahead picked up slightly in April, supported by a sustained recovery in new orders, positive signals for sales pipelines, and anticipated interest rate cuts in the second half of 2024.”